House Price Index: November 2025

Adapted from Zoopla’s House Price Report by Richard Donnell, Executive Director-Research 28 November 2025

With the Budget uncertainty now lifted, buyers and sellers can return to making decisions about their next move. Removing the threat of a new annual property tax from 210,000 homes for sale will help revive market activity in higher-value areas. However, the lack of any stamp duty reform means homebuyers will continue to face rising purchase costs.

Key takeaways

- House prices in southern England have dipped for the first time in 18 months

- Prices elsewhere are still rising by up to 3%, helped by steady supply and better affordability

- The Budget delivered a lift for the South by scrapping the proposed annual property tax, removing a concern for around 210,000 homes on the market

- With no major tax changes, the market now has a clearer outlook, which should support activity in early 2026

- Stamp duty remains unchanged, meaning more buyers are nudged into higher tax bands, weighing on prices and making moving home less tempting

Average UK house prices: last 3 months

The average house price in the UK is £270,200 as of October 2025 (published November 2025). This is a rise of 1.3% or £3,340 over the past year.

House prices falling across southern England

House prices across southern England have begun to edge down for the first time in 18 months, creating fresh opportunities for buyers. Market activity has cooled slightly since the summer as budget speculation encouraged many to pause and reassess.

Elsewhere, momentum remains strong. Prices are rising by up to 3% in the North West and by 2-3% across northern England, Scotland and Wales, supported by steady demand.

Talk of potential new taxes on homes over £500,000 has had a greater influence in the south, where more than a third of properties for sale fall into this bracket. This, combined with wider market trends, has nudged prices lower and expanded choice for buyers. The number of homes for sale in southern regions is now 8 to 15% higher than a year ago, helping to create a clear buyers’ market. Although buying costs increased after the end of stamp duty reliefs in April 2025, mortgage rates have largely held steady.

In other parts of the UK, budget uncertainty has had far less effect. More accessible price points, improved affordability and stable or reduced stock levels are supporting continued price growth.

Overall, this UK House Price Index shows average prices are 1.3% higher than a year ago. This is similar to last month and only slightly below the 1.7% annual growth recorded last year.

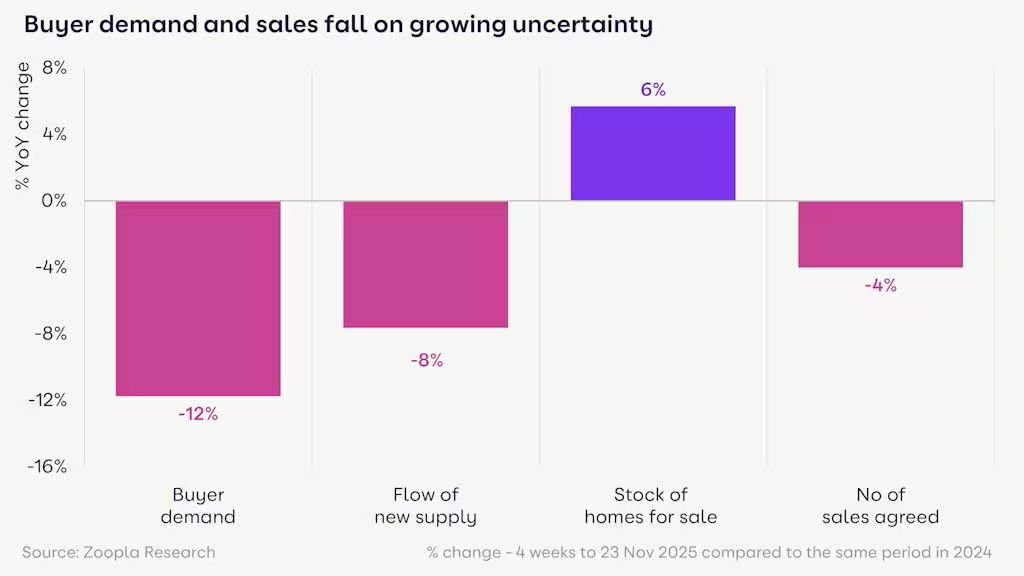

Buyer demand down 12% with sales agreed 4% lower

The seasonal slowdown has arrived a little earlier this year, with buyer demand sitting 12% below last autumn. Even so, the market is proving resilient. Sales agreed are only 4% lower than a year ago, as committed buyers press on to secure a deal before the year wraps up. Consider it the property market’s equivalent of getting the Christmas shopping done early.

Sales agreed to continue to offer the best snapshot of overall market health. Activity is slightly softer across most regions, with Eastern England seeing the largest fall at up to 9%. Yet there is plenty of stability too, with sales agreed holding firm compared with last year in Scotland, the East Midlands and Yorkshire & the Humber.

Post-budget boost for southern England in 2026

The standout housing announcement in the Budget is a new tax aimed solely at the highest-value homes over £2 million, touching just the top 0.5% of properties.

For the wider market, there is welcome relief. The removal of the potential annual property tax on homes bought for more than £500,000 provides a clearer footing for both buyers and sellers.

More than 210,000 homes are currently listed above this price point, making up around a quarter of all UK sales listings. These properties are largely concentrated in southern England and represent half of all homes for sale in London.

With this new clarity around future property taxation, confidence should begin to rebuild. After nearly four months of slower activity in late 2025, we expect the market to gain fresh momentum as we move into 2026.

Stamp duty is adding to costs for homebuyers

The Budget left stamp duty land tax unchanged, even though many argue that removing it could help boost home moves and support wider economic growth.

Stamp duty thresholds for main residence purchases in England and Northern Ireland were last updated in 2014. Since then, house prices have climbed by 47%, bringing more buyers into the stamp duty bracket and increasing the proportion of the purchase price that goes towards SDLT.

While lower stamp duty costs tend not to affect activity, higher charges can make households less inclined to move and can influence the prices buyers are prepared to pay, ultimately shaping price inflation.

First-time buyer reliefs continue to cushion the impact in most regions. Even so, more than half of first-time buyers in southern England now pay stamp duty, rising to 80% in London, compared with fewer than 10% elsewhere in the UK.

For existing homeowners, who do not benefit from reliefs, stamp duty is a routine part of moving. Over 90% of buyers across southern England and the Midlands pay SDLT, with the cost highest in areas where property values have grown the most.

A third of buyers now pay more than 2.5% of the purchase price in stamp duty

A decade of frozen stamp duty thresholds has quietly created fiscal drag, meaning buyers are paying more simply because house prices have risen while the bands have stayed the same.

Our analysis of sales agreed by existing homeowners in 2019 and 2025 highlights how this has shifted the landscape. The share of buyers paying higher effective stamp duty rates has jumped, with more than a third now paying over 2.5% of the purchase price, compared with just a fifth in 2019. At these levels, stamp duty is playing a growing role in how people price homes and in how willing they are to move.

In many southern towns, buyers of average-priced homes are now paying 3% or more in stamp duty. For instance, that equates to around £9,500 (2.5%) in Aldershot and £10,650 (2.6%) in Crawley. Against this backdrop, the case for abolishing stamp duty as part of broader tax reform remains compelling.

Market outlook

After months of anticipation, the Budget has proved gentler on the housing market than many expected. Buyers and sellers alike will welcome the clarity it brings, drawing a line under the uncertainty that has held back activity since late summer.

Our data shows that the underlying motivation to move home remains firm. With clearer direction now in place, we expect activity to pick up steadily as we head into the new year, with many households that delayed decisions returning to the market with renewed confidence.

The current gap in price inflation between the South and the rest of the UK is likely to continue. Sustained income growth will be essential in improving affordability and helping more households make their next move.

To view the report in full, please click here

How to Contact Us for Advice

Phil Clark will personally deal with your enquiry

Tel 0117 325 1511

Email info@swmortgages.com

Complete a form via our website www.bristolmortgagesonline.com

Please remember: YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE