Help to Buy Equity Loan & Shared Ownership

Caz Blake-Symes • July 20, 2020

Call us today for more information.

The Help to Buy Scheme

You only need a 5% deposit thanks to Help to Buy, and with the recent changes to Stamp Duty, it is so much easier to get the home you want for less. Start your search now and Contact Us today for help with financing your purchase.

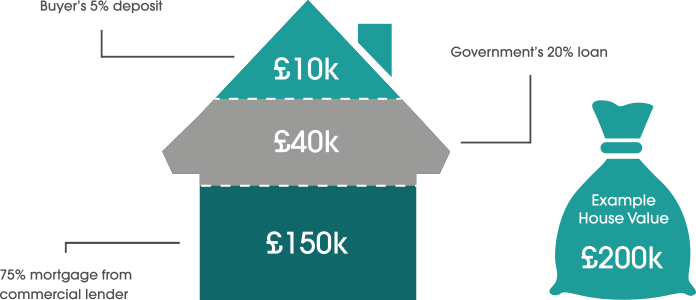

Help to Buy Equity Loan

- With an Equity Loan the Government lends you up to 20% of the cost of your newly built home, so you will only need a 5% cash deposit and a 75% mortgage to make up the rest.

- You will not be charged loan fees on the 20% loan for the first five years of owning your home.

- Equity loans are available to first time buyers as well as homeowners looking to move.

- The home you want to buy must be newly built by a Help To Buy accredited Builder, with a price tag of up to £600,000.

- You will not be able to sublet this home or enter a part exchange deal on your old home.

- You must not own any other property at the time you buy your new home with a Help to Buy: Equity Loan

In the Budget 2018 it was announced that the Help to Buy scheme would be coming to an end in March 2023. A new version of the Help to Buy scheme will operate from 1 April 2021 until 31 March 2023 which introduces changes to ensure the scheme is better targeted towards those who most need support to achieve home ownership. The key changes are:

- The scheme will only be available for first time buyers, defined as those who have not previously owned or purchased property.

- The scheme will introduce regional property price caps based on local markets, which will set the maximum price of a new build home that can be bought with Help to Buy in any region.

The regional caps are set out in table below:

Price cap for properties eligible for Help to Buy Equity Loan scheme from April 2021 to March 2023

North East £186,100

North West £224,400

Yorkshire & The Humber £228,100

East Midlands £261,900

West Midlands £255,600

East of England £407,400

London £600,000

South East £437,600

South West £349,000

Until the new scheme is introduced customers will continue to be able to purchase homes through the current Help to Buy scheme unaffected. However, all homes purchased under the current scheme will need to reach legal completion by 31 March 2021. This will influence when a builder will close for reservations using the scheme, therefore we recommend that you factor this into your plans and enquiries.

Shared Ownership

If you can’t quite afford the mortgage on 100% of a home, Help to Buy: Shared Ownership offers you the chance to buy a share of your home (between 25% and 75% of the home’s value) and pay rent on the remaining share. Later, you could buy bigger shares when you can afford to.

You could buy a home through Help to Buy: Shared Ownership in England if:

- your household earns £80,000 a year or less outside London, or your household earns £90,000 a year or less in London

- you are a first-time buyer, you used to own a home but cannot afford to buy one now or are an existing shared owner looking to move.

With Help to Buy: Shared Ownership you can buy a newly built home or an existing one through resale programmes from housing associations. You will need to take out a mortgage to pay for your share of the home’s purchase price, or fund this through your savings. Shared Ownership properties are always leasehold.

Only military personnel will be given priority over other groups through government funded shared ownership schemes. However, councils with their own shared ownership home-building programmes may have some priority groups, based on local housing needs.

People with disabilities

Home Ownership for People with Long-Term Disabilities (HOLD) can help you buy any home that is for sale on a Shared Ownership basis if you have a long-term disability. You can only apply for HOLD if the properties available through the other home ownership schemes do not meet your needs, eg you need a ground-floor property.

Older people

You can get help from another home ownership scheme called Older People’s Shared Ownership if you are aged 55 or over. It works in the same way as the general Shared Ownership scheme, but you can only buy up to 75% of your home. Once you own 75% you will not have to pay rent on the remaining share.

For further details about the service we offer as a fully independent mortgage brokers or any other mortgage information book your FREE CONSULTATION with one of our expert Mortgage Advisers please contact us.

Bristol Mortgages Online www.bristolmortgagesonline.com

Tel 0117 325 1511

Bath Mortgages Online www.bathmortgagesonline.com

Tel 01225 584 888

Exeter Mortgages Online www.exetermortgagesonline.com

Tel 01392 690 888

Email info@swmortgages.com

If there is one thing we know about the property market, it's that it never stands still. Over the last two decades, we have seen everything from global financial shifts and a pandemic that completely rewrote the rules of house hunting to fluctuating interest rates and evolving lending rules.

When your current mortgage deal is coming to an end, the ticking clock can feel a little intimidating. Do you stick with your current lender out of convenience, or do you dive into the endless sea of comparison sites to find something better?

For many homeowners, remortgaging is the single biggest opportunity to slash

This latest edition of our newsletter includes the following articles

Remortgage v Product Transfer

Why Choose an Expert Mortgage Broker

The perfect Partner for First-time Buyers

Helpful Mortgage Products from the Family Building Society

Time to Remortgage?

Plus lots more..

Click here to check it out.

Getting onto the property ladder-or even moving up it-can feel like an uphill battle in today's market. Between rising property prices and strict lending criteria, many buyers find themselves just short of the finish line.

At Bristol Mortgages Online, we pride ourselves on finding innovative solutions for our clients.

The UK property market moves fast, and sometimes the perfect opportunity doesn't wait for your current house to sell. Whether you’re a homeowner looking to secure your next dream property before selling your current one, or a developer eyeing an auction property that needs a quick turnaround, traditional mortgages ofte

Buying a home is likely the biggest financial commitment you will ever make. Whether you are a first-time buyer stepping onto the ladder, a homeowner looking to remortgage, or a seasoned investor expanding a buy-to-let portfolio, the process can often feel like a maze of jargon, paperwork, and fluctuating interest rate

Taking that first step onto the property ladder is one of the most exciting milestones of your life—but let’s be honest, it can also feel like navigating a maze blindfolded. Between deposit requirements, credit checks, and legal jargon, the process is daunting.

Recent global developments, including escalating tensions in the Middle East, have started to influence financial markets and, in turn, UK mortgage rates.

Understanding how these events filter through to borrowing costs can help you make more informed decisions.

If your current mortgage deal is coming to an end, you’ve likely started hearing the words "remortgage" and "product transfer" thrown around. In today’s shifting economic climate, making sure you are on the best possible mortgage rate is more important than ever.

we enter 2026, mortgage affordability remains one of the biggest concerns for homebuyers and homeowners alike. With interest rates, living costs, and lending criteria continuing to evolve, understanding what lenders look at when assessing affordability is more important than ever.